Consorcio Ara – Analysis and Valuation 2.0

At first glance Consocio Ara looks incredibly cheap, in this analysis I revisit the company to determine if it is really a great opportunity, or a value trap.

30 minute read

Introduction – Reason to Revisit the Company

In October 2023 I published a deep dive on Consorcio Ara, where I analyzed and valued the company to determine if it was an attractive investment opportunity. At the time of my writing, the company sold at a share price of MXN$3.4.

I was initially attracted to the company because the market valued it at a multiple of 0.3 times book value, placing a discount of 78% on current home inventory, valuing long-term inventory at zero, and land bank at cost. At a first glance, this seemed incorrect, Consorcio Ara had negative net debt, was profitable, generated free cash flow to the firm, and owned valuable tangible assets.

During my analysis I found out that the company’s housing business generated very poor returns on invested capital. Furthermore, capital could be locked up in land for many years. These factors led me to think that the company would perpetually destroy value. A reason to dismiss an investment in the company.

Another reason to pass on the company as an investment was that I did not fully understand the working capital requirements of the company, and thus could not have certainty on the continued availability of the dividend and earnings power.

Between then and now I have realized that any company at a price can be a buy. A mediocre business can be appropriately discounted to reflect its poor returns, and at a low enough price can be an opportunity. This does not mean that an investment in a bad business at a cheap price is a good long term investment. Rather, it is a way to capitalize on short to mid term correction of the multiple that the market places on the company. It is important to mention that value traps exist, and bad businesses burning through cash can quickly reduce the gap between price and value. To mitigate this risk when no catalyst is present, like in the case of Consorcio Ara, it is critical that the company’s intrinsic value is not eroding.

Consorcio Ara is not leveraged and produces free cash flow, so a risk of erosion between the value today and in the future is low. Cash is not being burnt, real estate inventory can be sold in a 2 year period, and the company’s land and commercial properties appreciate with inflation. These factors protect us from not having a catalyst, like a liquidation, to materialize the value of the company.

In Q4 2023 Hurricane Otis hit Acapulco, greatly damaging the city, where in 2023 15% of the company’s revenue came from. It is likely that the company will struggle to sell the remaining inventory in these developments in the near future. In view of this, management canceled its dividend. This has caused the company’s stock to decrease almost 16% year to date.

In this article I will revisit my analysis on the company and value it conservatively, considering the poor returns that the business generates, to determine if it is an attractive investment opportunity.

Investment Thesis

Inversion

I will take an inverse approach to analyze a potential investment in Consorcio Ara, by laying a hypothesis I can identify the key variables that would make an attractive opportunity.

Thesis

The company has negative net debt, is not at risk of financial distress, and is not burning through its cash balance to sustain operations.

The company’s real estate inventory has value. The company earns a low return on invested capital relative to the return available to investors, yet it is a profitable business.

The company holds commercial malls carried at cost in its balance sheet. These properties are worth more now because they were built a decade ago, and NOI is higher today than when they were built.

The company holds a valuable land bank carried at cost that was purchased more than a decade ago.

The company offers a dividend equivalent to a significant percentage of net income.

At a price of $X, I am getting $X in cash, $X in real estate inventory, $X in land, $X per share in commercial malls, minus all liabilities of $X, equals $X in net tangible assets. The intrinsic value of the company is unlikely to erode because the company is not leveraged and generates free cash flow. Finally, while I wait for the company’s valuation to correct, I will receive a dividend.

Key Variables

Value of real estate inventory

Valuation:

Present value of discounted real estate inventory to reflect poor rates of return.

Value of land bank

Valuation:

Land bank plus applicable appreciation.

Value of commercial malls

Valuation:

NOI after tax discounted by an appropriate cap rate.

Business is profitable, and will not erode margin of safety by burning through cash

Analysis:

Cash balance vs debt over time

Free cash flow (with maintenance capex) over time

Presence of nominal pricing power (cost inflation vs increases in home prices)

Renewal of dividend

Analysis:

Dividend paid and payout ratio over time

Management intent on renewing the dividend

Overview of Business

Consorcio Ara is a vertically integrated Mexican home builder. The company is family owned and operated. German Ahumada, the CEO, and his brother Luis Ahumada, who runs the commercial properties division, own a combined 48.6% of shares outstanding.

The company operates in 3 types of home segments–affordable, middle, and residential.

In 2023, the average price for affordable, middle, and residential homes was $40,000 USD, $70,000 USD, and $160,000 USD, respectively. 49% of homes sold were in the affordable category, 37% in the middle level, and 14% in the residential segment. Revenue from affordable, middle, and residential homes represented 33%, 38%, and 28%, respectively.

In Q1 2024, the company had a land bank of 32 million square meters, of which 30.8 million square meters will be used to build ~117,533 homes, and 2 million square meters for industrial or commercial or tourism projects. Most of the company’s land bank was purchased a decade ago and is carried at cost.

In addition to home building, the company operates 6 different shopping centers–205,275 m2 of gross leasable area with an occupancy rate of 94.7%. These shopping centers are close to the company’s real estate developments. In 2023 these shopping centers generated a NOI of MXN$303 million.

The company’s core housing business generates low returns on invested capital, yet it holds significant land and inventory in progress. Finally, its commercial real estate division generates an important amount of free cash flow.

Life Cycle of Homebuilding

Land Acquisition

The company invests capital to purchase land

Development and Construction

The company invests capital to convert raw land into sellable housing units. These investments include urbanization costs, construction materials, permits, labor, and construction costs, and are reflected in inventory in progress.

Sales and Marketing

The company spends capital in marketing the project, and in agent commissions to sell the properties.

Project Completion and Handover

Final payments from buyers upon completion and handover of the property.

The company recognizes the revenue from the sale of the property.

The hardest part in the process to build a real estate project is acquiring the land. According to the CEO of Casas Acre, acquiring the land for the project and getting the permits is 80% of the work.

Working Capital Needs

Capital can be tied in land, development, and construction phases. Capital tied up in land has the benefit of appreciation and preservation, even if it is not being used.

The overall efficiency of the company’s operations can be measured by looking at the Cash Conversion Cycle, which reflects the number of days that capital is tied up in inventory and accounts receivables. They key components in understanding a home builder’s cash conversion cycle are:

Inventory Days: Time taken from the start of construction to the sale of the project.

Receivable Days: Time taken to collect payment from buyers after the sale.

Payable Days: Time taken to pay suppliers and contractors.

The earnings capacity of a home builder is tied to their inventory in progress, which represents the projects that they are developing. We can conceptualize the working capital needs of a home builder through investment cycles. As soon as one project is done, the life cycle of a project ends, and the home builder has to invest capital to start a new one.

In the case of Consorcio Ara, the company has a very large land bank–enough to build ~119,607 homes–which means that new investments for land acquisition should be minimal and the company should be able to continue to make housing projects going forward.

Analysis of Operations – Home Building

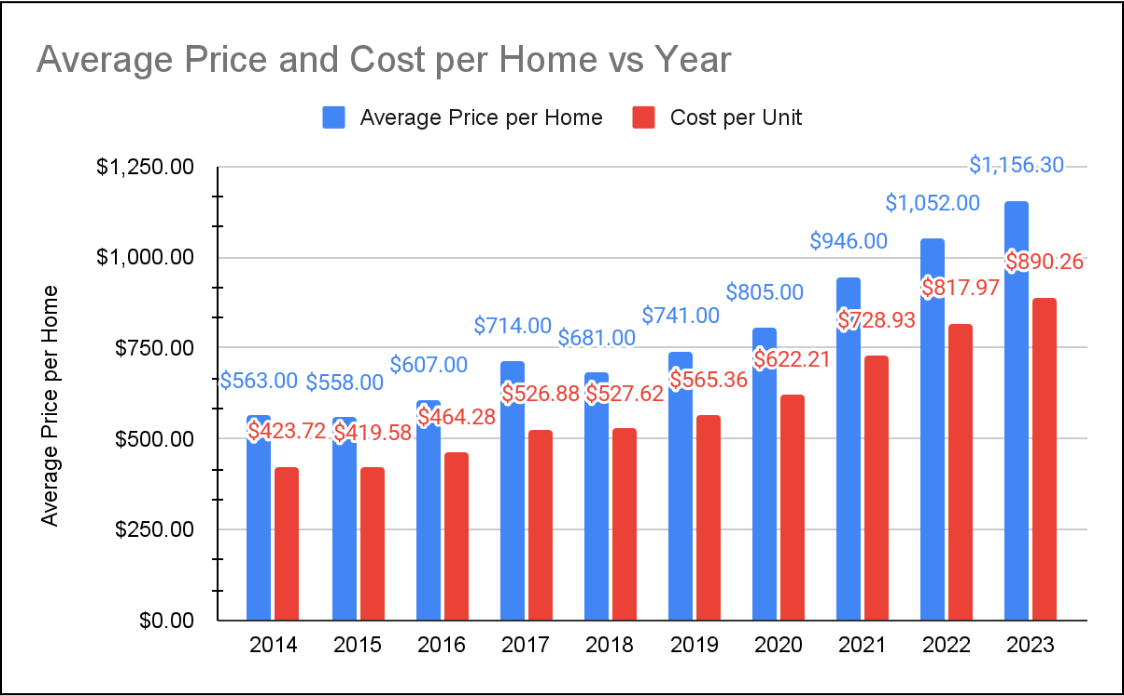

The following graph illustrates the company's operations from its housing business from 2014 to 2023. In 2023 the company generated MXN$6,444 million in revenue from this division.

The production of homes radically decreased from 11,400 to 6,500 between 2018 and 2020 as a result of reduction in subsidies and stricter credit requirements to obtain a loan from Amlo´s administration.

The company has been able to maintain historic revenue levels by switching strategy to sell higher value homes, and passing on inflation to consumers. From 2018 to 2023, the average price per home that the company sold increased 69% vs an increase of 68% in cost inflation vs an increase in CPI inflation of 34%–reflecting nominal pricing power.

To add on, between 2018 and 2023 the company’s strategy to sell higher value homes meant building vertical housing complexes and increasing the production of homes in the middle category.

The following graph displays an important reduction in revenue from affordable housing. In 2018, 44.1% of revenue came from developments in the affordable housing sector, vs 29.5% in 2023.

In Q1 2024, income from the affordable segment increased 32%, as a result of the opening of a development that in Q4 2023 struggled to receive a permit. Moreover, revenue from the residential segment experienced a decline of 44% due to lower sales from a development in Acapulco. The company is suffering from lower sales in Acapulco due to the damages of Hurricane Otis. For context, in Q1 2023 sales from developments in Acapulco represented 16.3% of revenue from housing, vs 8.4% in Q1 2024.

The company’s operating efficiency also changed between 2018 and 2023 as a result of the strategy to develop more mid and residential housing. The following graph illustrates how the time to build and sell a project changed from 676 days in 2018 to 818 days in 2023.

A figure of 818 inventory days means that capital is tied up for 2.24 years in the investment cycle. This number helps us understand the value destruction of the company’s housing business by comparing the return on investment during this period vs the return available to shareholders.

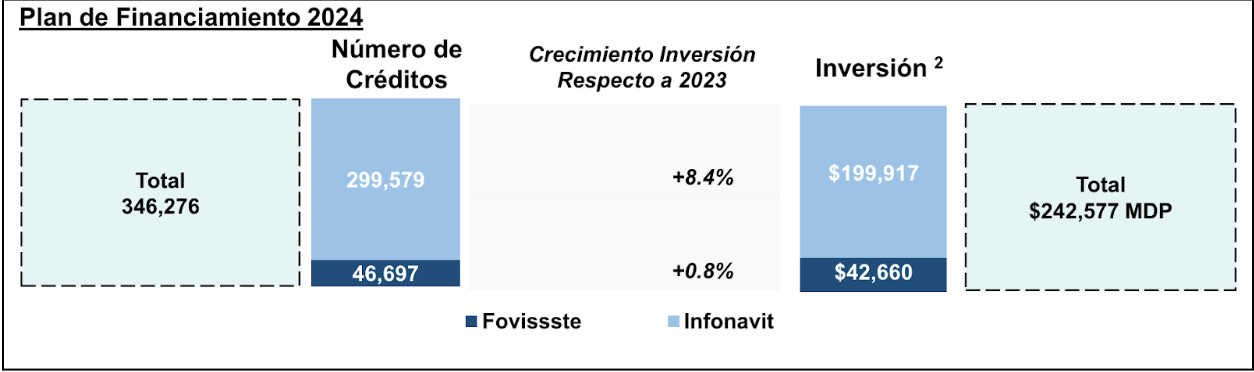

The company’s housing business depends on financing from government institutions. In 2023, 59% of customers financed their home purchase with a credit from Infonavit, and 16.7% with a credit from FOVISSSTE. Only 23.3% of customers financed their purchase with a credit from bank institutions.

Significant dependence on government financing for home purchases is a risk for the company, as policy changes can have a dramatic effect on operations, as seen in 2018. For 2024, financing from INFONAVIT is expected to increase by 8.4% relative to 2023, and remain stable for Fovissste.

This level of financing from government institutions should cause home sales to remain stable in 2024 relative to 2023.

Analysis of Operations – Commercial Malls

Properties

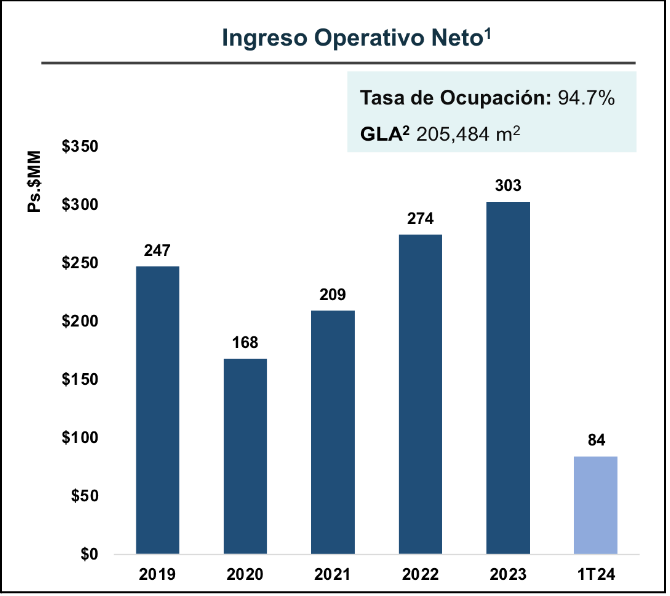

As of 2024, the company has 205,484 square meters of gross leasable area with an occupation rate of 94.7%. In 2023 the company’s commercial properties generated a NOI of MXN$303 million.

Consorcio Ara owns 100% of 4 four commercial malls and other unicenters and minicenters. These commercial malls include: Centro San Miguel, Plaza Centella, Centro Buenaventura, Plaza Carey.

The company also owns 50% of two commercial malls: Centro las Américas and Paseo Ventura. Centro las Américas was built in 2005 and is located in the outskirts of Mexico City in Ecatepec, near a housing development.

The company has continued to invest in expanding its commercial properties. In 2022, the company invested $172 million to expand Plaza Centella GLA by 3,000 square meters. This same year, the company invested capital to expand Centro las Américas.

In 2022, co-owned commercial properties generated MXN$182.9 million in net income, of which MXN$108 million was attributable to Consorcio Ara.

NOI

The following graph illustrates the company’s NOI from wholly owned commercial properties plus the participation in co-owned properties.

Valuation

In 2022, the company stated that according to an independent auditor, the reasonable value for its wholly owned commercial properties was MXN$2,932 million, compared to their book value of MXN$1,065 million.

Given a NOI of MXN$303 million, a capitalization rate of 11%–which represents the return shareholders can receive elsewhere–and a tax rate of 30%, I estimate the value of the company’s investment properties at MXN$1,928 million = (303*0.7)/0.11. This figure is 37% above the book value of these assets. Compared to the valuation of the independent auditor, which does not include the company’s partially owned commercial properties, my estimate is very conservative.

Profitability of Operations

Margins

The following graph shows the profitability of Consorcio Ara’s housing and consolidated operations from 2014 to 2023.

In 2023, gross margin per housing unit was 23%, vs the consolidated gross margin of 26.5%. The gross margin per unit is lower because the consolidated figure incorporates income from commercial properties.

It is important to highlight that gross margin per housing unit remained stable between 2014 and 2023. As for the operating margin, figures have were fairly stable between 2019 and 2023 (ignoring 2020). Overall, these results indicate that the operations of the business are stable, and future results should be similar to current ones if the company decides to remain in the housing business.

Change in Non-Cash Working Capital

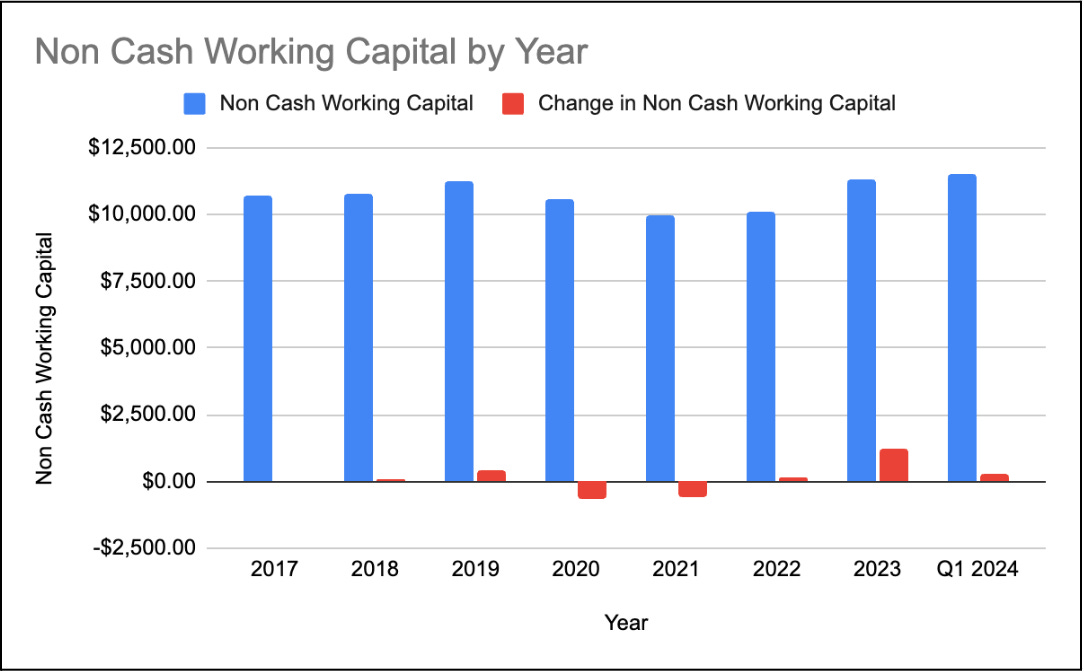

The following graph illustrates non-cash working capital levels between 2017 and Q1 2024.

Non-cash working capital remained fairly stable between 2017 and Q1 2024. In 2023 non-cash working capital increased by $1,207.3 as a result of investments in current housing projects, leading to negative free cash flow. Management has stated that they plan to focus on generating positive free cash flow in 2024, indicating that they will be more restrictive in expanding real estate inventory.

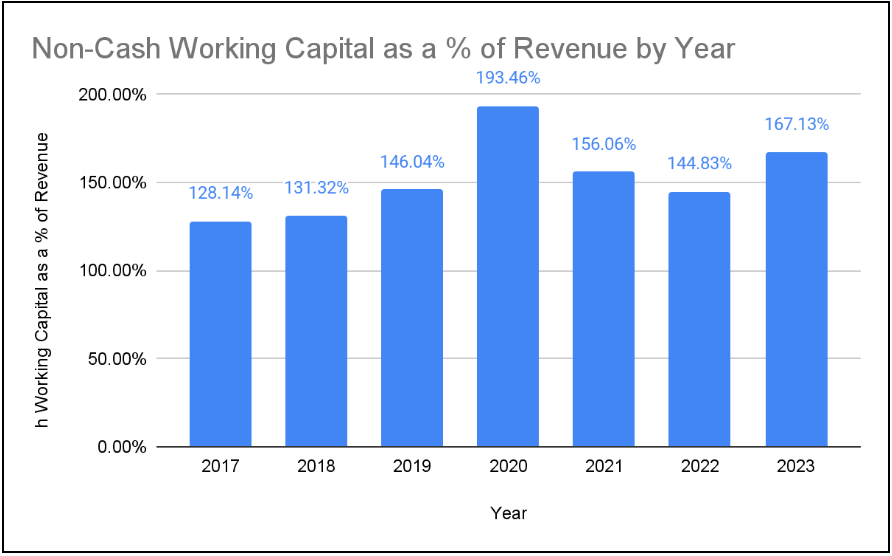

It is also important to compare non-cash working capital to revenue to understand how much capital the company needs to tie up to generate every $1 of revenue. The following graph displays non-cash working capital as a % of revenue from 2017 to 2023.

Since 2019, when the company switched strategies to sell more homes in the middle segment, the company has needed to tie more capital for every $1 of revenue, reflecting a less efficient operation. On average, between 2019 and 2023, and excluding 2020 because of the pandemic, the company’s non-cash working capital as a percentage of revenue was 153%.

Invested Capital

The following graph shows how the company’s consolidated and per division invested capital have changed between 2017 and Q1 2024. Invested capital in the housing division has remained fairly stable during this period. On the other hand, invested capital in the commercial properties division increased 53.6%.

ROIC

The following graph shows the company’s consolidated and per division return on invested capital. In 2023, ROIC from the housing and commercial properties division was 3% and 15.2%, respectively.

The return on invested capital from the housing division is significantly below the return available to shareholders elsewhere–the current Mexican fed rate is close to 11%. As a result, invested capital in this division, which mostly constitutes real estate inventory, should be discounted to reflect the poor returns that it generates.

Free Cash Flow to the Firm

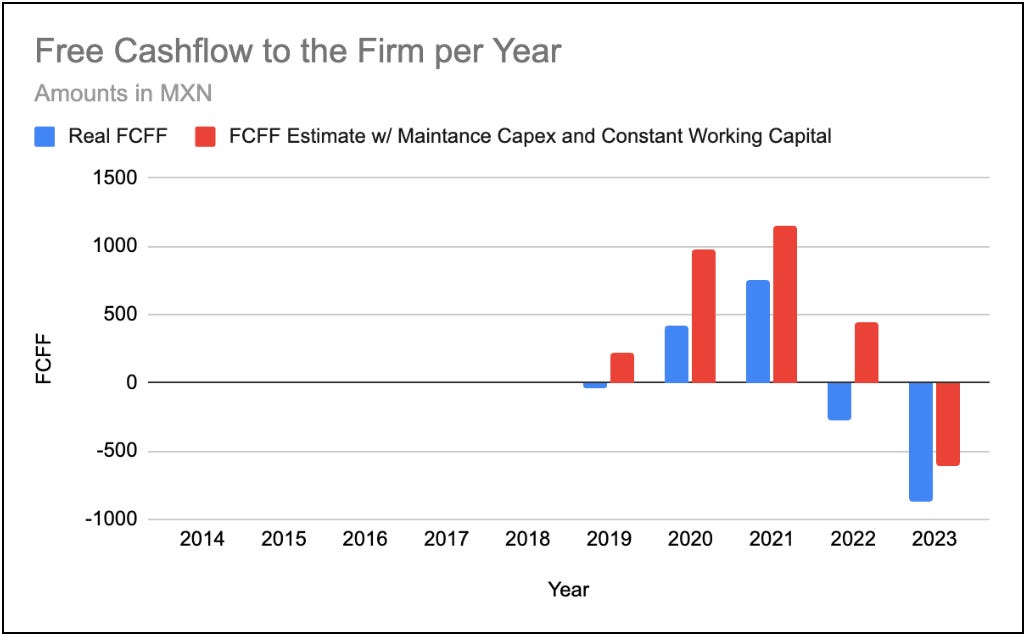

The following graph displays the company’s free cash flow to the firm from 2019 to 2023. We observe a significant difference between the Real FCFF and the FCFF estimate with maintenance capex and non-cash changes in working capital. The principal cause for the difference in amounts is that my estimate of FCFF does not incorporate cash outflows for land acquisitions nor increases in long term real estate inventory.

Between 2019 and 2023, Consocio Ara invested a total of MXN$296 million in new land parcels, and MXN$1,888 million in long-term real estate inventory. These investments represent cash outflows that have reduced free cash flow.

The company discloses little information about investments in long term real estate inventory.

During this period, the company generated a total real FCFF of MXN$16.6 million, and a FCFF excluding investments in long term real estate inventory and land acquisition of MXN$2,178 million.

Consorcio Ara is not burning through cash to sustain operations, nevertheless, its capital allocation decisions are very poor. The company re-invests a large percentage of the income from its housing division back into long term assets like land that lock up the capital for many years. Land does not depreciate with inflation, but generates very poor returns once used for housing development, even after waiting many years.

Considering this, both real estate inventory and land must be discounted appropriately to reflect the poor returns that the capital tied up in these assets will generate.

Cash Balance vs Debt

The following graph shows how the company’s cash, total debt, and net debt positions have changed between 2017 and Q2 2024. The company has historically maintained a very healthy balance sheet, with minimal levels of net debt. A built up of cash between 2017 and 2022 supports the argument that the company does not burn cash to sustain operations.

In 2023, the decrease in cash was attributed to extraordinary land purchases and increases in working capital real estate inventory.

Net Asset Value Valuation (as of 2Q 2024)

Cash: MXN$2,294.9 million

+ Account Receivables: MXN$785.4 million

+ Real Estate Inventory

Book Value: MXN$12,242 million

Short Term Real Estate Inventory: MXN$11,052 million

Land: MXN$1,190.4 million

Adjustment for Low Returns on Invested Capital

The company’s housing business generates very poor returns on invested capital relative to the returns available to investors. As a result, real estate inventory, which comprises most of invested capital, must be discounted to reflect the destruction in value. A destruction in value occurs because the company could have invested this capital at better returns.

For example, $100 invested in a checking account that generates 3% annual return will be worth $103 at the end of the year. However, if during the same period investors had the option of choosing a different checking account that generated a return of 10%, then they could achieve the same result of $103 at the end of year 1 by investing $93.6. So, investors that chose to invest their money at 3% destroyed $6.4 in value because at the available return, the present value of their $100 invested at 3% is $93.6 (100 *1.03 /1.10).

Following this same logic, the company’s real estate inventory must be discounted to reflect the destruction in value from the poor returns it generates.

My adjustment for value destruction assumes that Consorcio Ara will continue to invest in similar housing projects, maintain similar levels of working capital and achieve a ROIC of 3%.

To adjust the company’s real estate inventory, I will use a cyclical method of discounting that considers a time frame of 10 years and a period of 2 years per investment cycle. This method will project the future value of inventory at the current ROIC for each 2-year cycle (time taken to sell real estate inventory) and then discount it back to the present value using the opportunity cost. I believe this method is most appropriate because it reflects the repeated impact of poor returns over multiple cycles.

Future Value of Inventory at ROIC for One Cycle:

Future value of initial inventory value after each 2 year cycle

FV = 12,242 * 1.03^2

FV = MXN$12,987.53 million

Discount Future Value to Present at Opportunity Cost

Present value (PV) after each 2-year cycle

PV =12,987.53/(1.1^2)

PV = MXN$10,733.5 million

Value Destruction per Cycle

Value Destruction = Initial Inventory Value - PV

Value Destruction = 12,242 - 10,733.5

Value Destruction = MXN$1,508.5 million

Discount Value Destruction Back to Present Value

For each cycle in a period of 10 years, I will discount the value destruction back to the present.

Year 2: PV = 1,508.5/(1.1^2) = MXN$1,246.69 million

Year 4: PV = 1,508.5/(1.1^4) = MXN$1,030.32 million

Year 6: PV = 1,508.5/(1.1^6) = MXN$851 million

Year 8: PV = 1,508.5/(1.1^8) = MXN$703 million

Year 10: PV = 1,508.5/(1.1^10) = MXN$581 million

Cumulative Present Value of Value Destruction in 10 Years

Cumulative PV = 1,246.69 + 1,030.32 + 851 + 703 + 581

Cumulative PV = MXN$4,412 million

Subtract Cumulative Value Destruction from Real Estate Inventory

Adjusted Value of Real Estate Inventory = 12,242 - 4,412

Adjusted Value of Real Estate Inventory = MXN$7,830 million

Discounting the value of the company’s real estate inventory to reflect its perpetual value destruction by continuing to employ this capital in housing developments, we find that the value of the real estate inventory is MXN$7,830 million. This figure is 64% of the stated book value, and it considers that the company will reinvest most of the capital back into its housing business after selling a project, thereby continuing the cycle of value destruction by putting capital to work at very low rates of return for many years.

+ Land Bank

Book Value: MXN$3,209.8 million

The value of the company’s unused land is accounted separately from the land currently used in real estate inventory.

Initially, I thought that the company’s land bank was significantly worth more than its book value because it is carried at cost and it was bought a decade ago. Nevertheless, I have come to realize that the value of the land bank is actually worth less or equal to the stated book value because the company will use most of this land for housing developments, which generate very poor returns on invested capital. So, as long as the company uses this land for housing developments, the stated book value of the land must be discounted to reflect the poor returns that it will generate.

On the other hand, an estimation of the company’s land bank at below book value could be excessive because it does not incorporate that the company holds real estate beachfront gems, and that the land bank includes 2 million square meters that will be used for industrial and tourism projects. Moreover, management has stated that they conservatively value its land bank at 1.4 book value, and that in 2014 banks estimated the value of the land bank conservatively at 1.9 book value.

Considering all of the points above, I think it is conservative enough to value the company’s land bank at book value.

+ Commercial Malls

Book Value: MXN$1,065 million

Estimate of Fair Value: MXN$1,928 million

+ Long Term Real Estate Inventory

Book Value: MXN$2,073 million

Estimated Value: MXN$1,036 million

The company discloses very little information about long term real estate inventory. To remain conservative, I will discount this asset by 50% because of future value destruction and the uncertainty of not knowing what this asset is compromised made of.

- All Liabilities: MXN$8,483 million

= Net Asset Value (NAV)

NAV = Cash + Account Receivables + Real Estate Inventory + Land Bank + Commercial Malls - All Liabilities

NAV = 2,294.9 + 785.4 + 7,830 + 3,209.8 + 1,928 + 1,036 - 8,483

NAV = MXN$8,601 million

Sum of Parts Valuation

To complement my net asset valuation, I will estimate the intrinsic value of Consorcio Ara by calculating and then adding together the company’s housing business, investment properties, and land bank.

Housing Business

On May 20 2024 Vinte, an established Mexican public home builder, made a tender offer to purchase Casas Javer at MXN$14.9355 per share or MXN$4,215 million for the equity part of the business. This offer was accepted by 64% of Javer’s shareholders, and approved on July 12 2024 by Vinte’s board.

Casas Javer is focused on the development of affordable homes. The company is more profitable than Consorcio Ara.

(2023 figures, in millions of MXN)

Homes Built: 12,201

Revenue: $8,904

Operating Income: $1,303

Net Income: $564

ROIC: 28%

Invested Capital: $4,509

Book Value: $2,741

Based on the price of the tender offer and 2023 figures, Vinte is paying a multiple of 7.4 times earnings and 1.6 times book value, to acquire the equity part of the business.

Prices Paid by Vinte & Valuation Multiples:

Shares Outstanding: 282,939,106

Equity Value: $4,215 million

Enterprise Value: $5,372 million

Book Value per Share: 9.61

EV/EBIT: 4

P/E: 7.4

P/B: 1.6

Javer is more profitable, justifying a higher multiple compared to Consorcio Ara. I believe a conservative figure for Consorcio Ara is around 5 times earnings. In 2023, Consorcio Ara’s housing business generated MXN$547 million in operating income. After tax, this figure is MXN$382 million. At this valuation, Consorcio Ara’s housing business would be worth MXN$1,910 million.

Land Bank

I think it is correct to consider Consorcio Ara’s land bank separately from its housing business because of its size. Although the company needs this land to operate and continue generating earnings from its housing business, today Consorcio Ara is overcapitalized in terms of land holdings.

Vinte’s tender offer to acquire Javer values the company at 7.4 times earnings, and this valuation includes the company’s land bank. Which is large enough to build 52,577 homes and support 4.3 years of operation. On the other hand, at current levels of home production, Consorcio Ara would take almost 20 years to use its land bank. Highlighting the excess land holdings of Consorcio Ara.

Consorcio Ara also owns valuable land parcels that will be used for non-housing development purposes.

Considering that Consorcio Ara is overcapitalized with land, a percentage of this land bank should be added in the sum of parts valuation. Not adding it would be illogical because the company could continue to invest in land, increasing this asset account, and the value of the housing business would stay the same and not account for this value.

To remain conservative, we will only add the land bank that is not part of current real estate inventory, as the land considered in inventory supports 5 years of operations (5 = (19.6 total years * 1,190 value of land bank in inventory)/4,368 total value of land bank)).

Value of Land Bank = MXN$3,209.8 million

Commercial Properties

As mentioned before, I estimate the value of the company’s investment properties at MXN$1,928 million.

Sum

MXN$7,047 million = $1,910 + $3,209.8 + $1,928

Analysis of Margin of Safety

Based on my NAV valuation, at a price of MXN$3,700 million, I am getting MXN$2,294.9 million in cash, MXN$785.4 million in receivables, MXN$7,830 million in real estate inventory, MXN$3,209.8 million in land, and $1,928 million in commercial malls; minus all liabilities of MXN$8,483 million, this equals MXN$8,601 million in net tangible assets.

Similarly, on a sum of parts basis, which uses a multiple of 5 times earnings to value the company’s housing business, plus excess land holdings, and commercial properties, I estimate Consorcio Ara’s intrinsic value to be MXN$7,047 million.

Based on my calculations, Consorcio Ara is conservatively worth between MXN$7,047 million and MXN$8,601 million.

These figures compare positively with the current market price of MXN$3,700 million, offering a 47% margin of safety and a potential upside of 90%, at the lower end.

The intrinsic value of the company is unlikely to erode because the company is not leveraged, is profitable, and does not burn through cash to sustain operations. The company’s main assets: land, real estate inventory, and investment properties also appreciate with inflation.

It is important to note that both valuations are very conservative–58% of book value at the higher end. My estimate of the company’s land bank assumes no appreciation, and real estate inventory was significantly discounted to reflect the poor returns that the business currently generates. Furthermore, my valuation of the company’s commercial properties is below the estimate of the company’s independent auditor. Moreover, the housing industry in Mexico is currently facing a difficult environment, which could improve given the demand for housing and change in government administration. An improvement could increase returns on invested capital and increase the value of real estate inventory.

Considering all of the above, an investment in Consorcio Ara at the current price offers an attractive return with minimal risk of losing money. My investment is protected thanks to the company’s unleveraged position and the tangible assets it owns. Meanwhile, while I wait for the company’s valuation to correct, I will receive a dividend between 4% to 5%. In the event that the market does not correct the company’s valuation, the cost of just holding the stock is reduced by this dividend payment.