How to Analyze Banks (part 1)

An introductory guide to help you understand future bank valuations.

15 minute read

Banks recently peeked my attention.

Earlier this year we saw the fall of three local banks in the US, namely SVB Financial Group, Signature Bank, and Silvergate Capital Corp. These banks previously held long-term, low-yield U.S. Treasury investments and experienced a swift decline in client funds, causing their operations to become untenable.

I did not know, but modern banks, in sharp contrast to non-financial companies, generally do not fail in normal times. The rate of bank failures in the US between 1935 and 1940 was about 0.5 percent per year, and it remained below 0.1 percent per year in the 20 years after World War II. Between 2001 and 2008, only 50 banks failed in the United States, half in 2008 alone.

Why is this?

Weak banks are conveniently merged into other, stronger banks

Banks are intertwined with other banks, meaning that if one fails, the other will likely follow, so the government has stepped in and provided bailouts

Deposit-taking institutions are rarely left to fend for themselves and go bust because it could trigger a systematic risk for other banks

In the midst of this analysis, several things happened:

I realized that I had forgotten how to analyze banks.

I visited Colombia and learned about a Colombian business group called Grupo Empresarial Antioqueño, composed of 3 conglomerates: Grupo Sura, Grupo Argos, and Grupo Nutresa. Grupo Sura is a financial conglomerate that owns 46% of Bancolombia, Colombia’s largest bank. Grupo Argos is an infrastructure and cement conglomerate that also, through its equity stake in Grupo Sura, owns Bancolombia. Both companies sell at attractive multiples, and Bancolombia specifically sells at a PE ratio of 3~.

Curious about the valuations of other Colombian banks, I learned that most banks in the country currently sell at earnings multiples of 3 - 4 times

In the next two months, my goal will be to analyze the Colombian banking sector, and Grupo Sura and Grupo Argos

Before that, it is necessary to revisit how to analyze banks, thus the objective of this article. I hope this article also helps you to understand how banks work.

How the banking business works

Overview

Banks take in money from depositors. This capital is labeled as a liability because it is money that the bank will have to return to the depositor in the future. In exchange for placing money with the bank, the bank will pay interest to the depositor.

The bank uses this capital to make loans with interest. Banks make money from the difference between the interest earned on loans and the interest paid out to depositors. This difference is considered net interest income.

What types of customers exist for a bank?

Banks can loan money to 4 main types of customers: individuals, businesses, financial companies, and governments.

What types of loans exist?

Secured loans. Secured loans refer to loans backed by collateral. A collateral is an asset that the lender has the right to obtain if the borrower does not pay back their obligation. Because collateral can normally be appraised with some degree of accuracy, the credit decision is simplified. As Roger Hale, points out, “If a pawnbroker lends money against a gold watch, he does not need credit analysis. He needs to know the value of the watch.”

Unsecured loans. Unsecured loans refer to loans that are not backed by collateral.

What types of deposits exist?

Demand deposits. Deposits that can be withdrawn at will without notice to the bank.

Time deposits. The depositor commits to leave funds with a bank for a specified period.

Savings deposits. A hybrid between a time deposit and a demand deposit. These include funds deposited into a savings account.

Generally speaking, the more access the depositor is willing to forego, the greater the rate of interest that can normally be obtained.

How are banks different from non-financial firms?

Overview

A bank’s liabilities are its “assets” or “raw material”. Banks use depositors’ money or debt to earn money, by making loans. This is very different from non-financial firms, where liabilities only constitute an obligation.

Moreover, in contrast to non-financial firms, which can choose to operate only with cash, banks cannot avoid credit risk. Credit risk is the risk of loaning money to someone and not paying it back. Success in banking thus depends on effectively selecting and managing risk.

Income Statement

A bank’s revenue can be divided into interest and non-interest income. Loans are assets that a bank uses to earn interest income. Some types of non-interest income include trading gains, and fees and commissions.

Generally, the most significant expense for a bank is interest expenses. As mentioned before, this refers to the interest paid to depositors and creditors from whom it has borrowed funds.

Net interest income is equaled to interest income - interest expense. This relates to the bank’s interest spread, the difference between the rate of interest charged to borrowers and the rate of interest paid to depositors. Net interest income is more important than each of its constituents–interest income and interest expense. Since each will typically vary depending on current interest rates, while net interest income will tend to be relatively less sensitive to change. Significant increases or decreases in net interest income are therefore more important to analyze. In general, consistent growth in net interest income, in line with asset growth, and somewhat above average to a bank’s peers, is ideal.

For a bank, net interest income + non-interest income is equal to operating income.

For most banks, compensation (salary and bonuses) are the largest single category of non-interest expense.

Operating income - operating expenses are equal to pre-provision income.

Banks make provisions against bad and doubtful losses regularly to protect themselves against loan defaults. These provisions are an expense in a bank’s income statement.

Pre-provision income - provision for losses - nonoperating items equals pre-tax profit.

The following diagram explains the above:

Balance Sheet

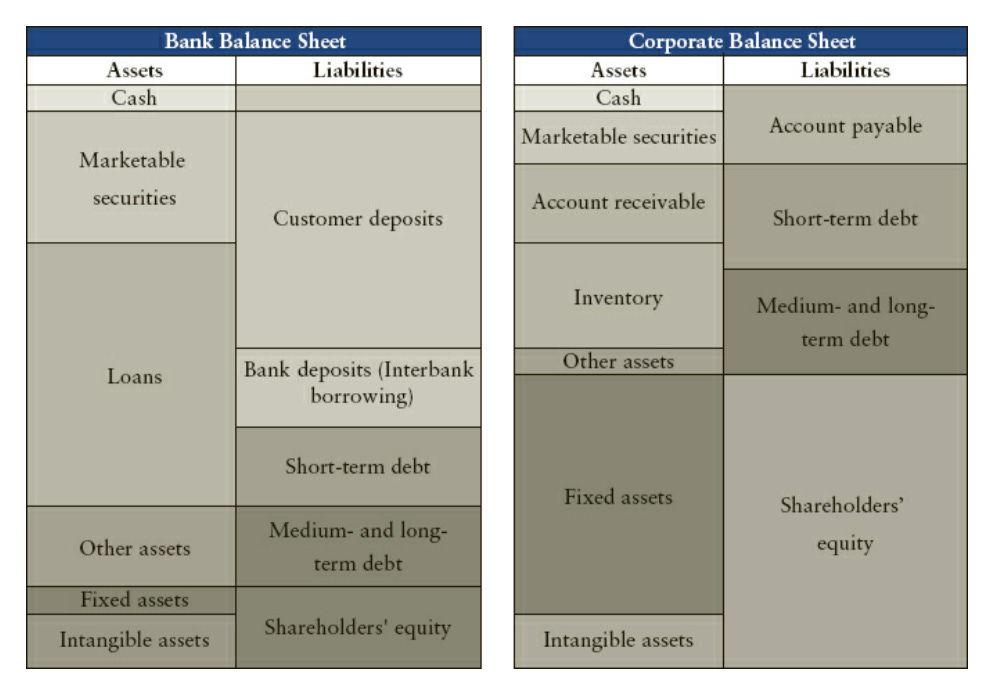

Superficially, a bank’s balance sheet is confusing and can communicate an alarming situation. Liabilities are mostly short-term (deposits), but most of its assets are long-term (loans), and it is highly leveraged (total liabilities to equity is high).

A bank’s assets mainly include cash, securities, and loans that the bank has made. On the other side, liabilities mainly include money taken from depositors and short-term debt.

Assets are normally listed based on liquidity in descending order. Cash, cash equivalents, and securities (including reverse repos) are the most liquid. Reverse repos are securities that a bank has purchased from another bank with the agreement that they will be bought at a premium at a later date. Less liquid assets include loans.

For the liability side, banks’ obligations mostly comprise customer deposits, interbank borrowing, and short-term debt.

When analyzing a bank’s balance sheet, it is important to know what percentage of funding comes from customer deposits.

Cashflow Statement

We understand that the cash flow statements record inflows and outflows on a cash basis. This is very important when analyzing nonfinancial companies but is of little use in analyzing banks and financial companies. This is because cash is a bank’s “raw material” and movements of cash do not represent financial performance. For example, if a depositor puts money in a bank, then that is an inflow of cash, but it does not mean that the bank earned that money. Consequently, the income statement, rather than the statement of cash flows, is the best financial report.

What are the key areas when analyzing a bank?

The key areas to understand the health and potential earnings power of a bank include its earnings capacity, liquidity (access to cash to meet obligations), capital adequacy (cushion that the bank’s capital affords vs liabilities to depositors and creditors), and asset quality (the likelihood that the loans the bank has made will be repaid).

In the next parts of this series, we will expand and understand the above.